There has been nothing to get excited about in the UK stock market recently. The FTSE 100 has been moving sideways, at best, for about three years.

In February last year I bought shares in a boring investment trust called Brunner. The Brunner family sold their chemical business to ICI in the 1920s and set up the trust to look after their money. Now anyone can invest in this stupendously dull fund. I paid £5.51 fifteen months ago and the shares are now limping along at £5.28. The fund holds shares in eighty companies: roughly a third in the UK, a third in North America and the rest in Europe, the Far East and Latin America. Four times a year it coughs up a dividend, about 2.8%. It has increased this dividend every year for the past forty-three years. One reason the share price is weak is that it is trading at a 12% discount to Net Asset Value. This is because the Brunner family still own 30% of the company making it an unlikely takeover target, like Caledonia. Boring as a wet Sunday afternoon at prep school but a pretty safe way to preserve capital and get a modest but growing income.

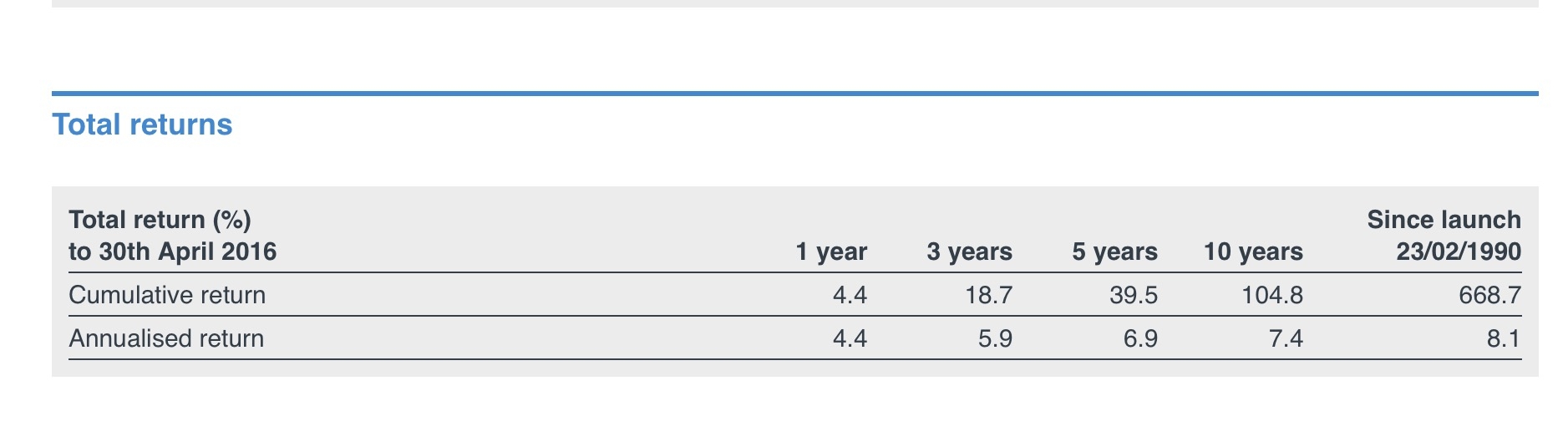

Meanwhile McInroy & Wood, who I periodically praise here, are not quite as dull as you might think. They differ from Brunner in that they invest in bonds as well as equities. In the last six months they have increased their holdings in bonds (mostly UK and US Treasuries) to 40%, reflecting their view that from moving sideways equities may break to the downside. If they are right they will outperform their peers with a greater exposure to equities. Their charges are higher than for an investment trust but they earn their fees, I hope, by this re-allocation of assets. They have been chugging along pretty impressively since 1990. Here is the record for their flagship Balanced Fund which yields 1.8%. The numbers assume that the dividends have been re-invested. Of course they haven’t, they have been spent paying the bills.